Your credit score is one of the most important factors for financial health in the US. Whether you’re applying for a mortgage, a car loan, or even another credit card, lenders use your credit score to assess your reliability.

One factor that heavily impacts your score is your credit card utilization ratio. This blog explains what it is, why the 30% rule matters, and how you can use it to improve your score.

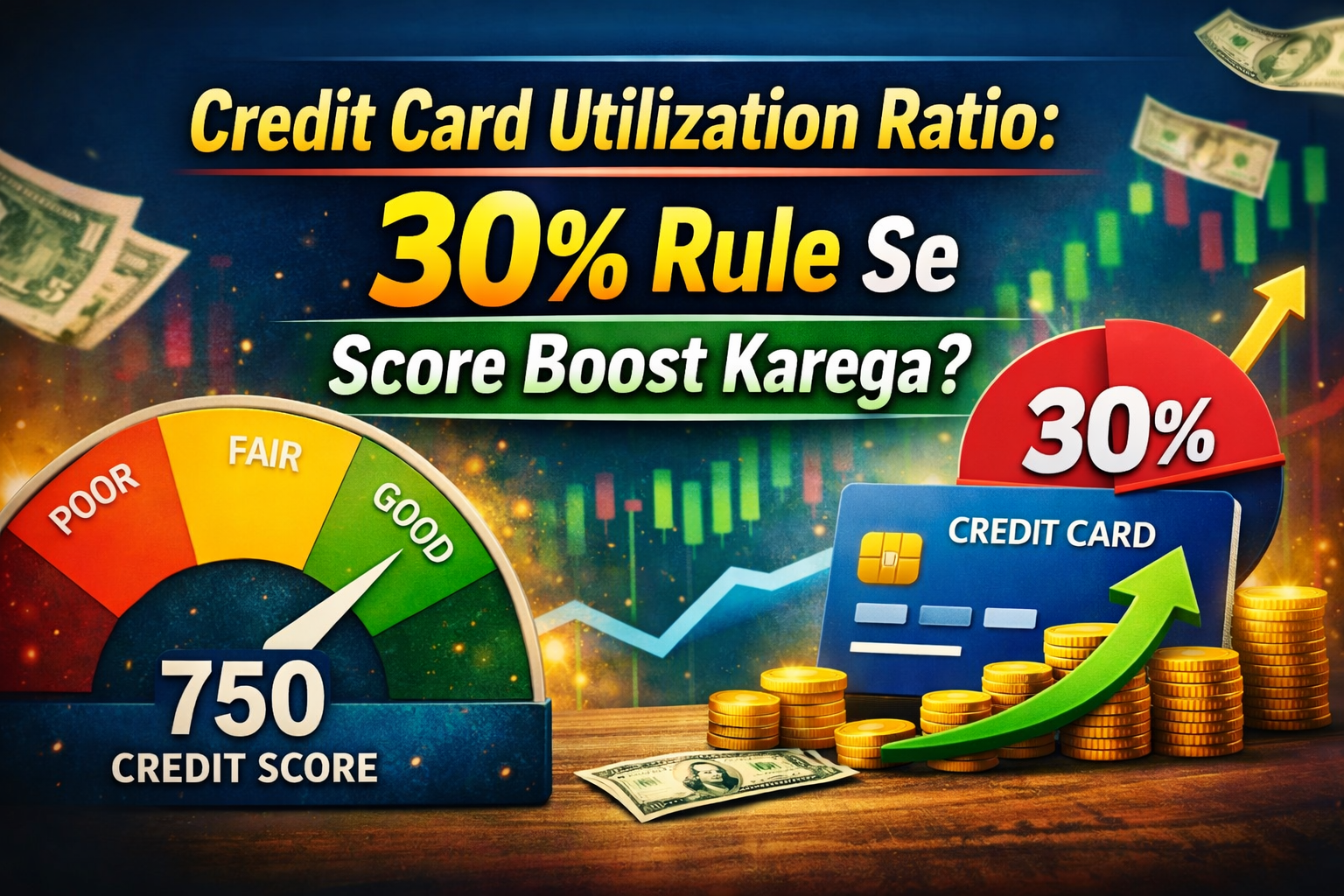

What Is Credit Card Utilization Ratio?

Credit card utilization ratio is the percentage of your available credit that you’re actually using. It’s a key component of your FICO and VantageScore.

Calculation:

Credit Utilization Ratio = (Credit Card Balance ÷ Credit Limit) × 100

Example:

If you have a total credit limit of $5,000 and your balance is $1,500:

1,500 ÷ 5,000 = 0.3 → 30%

30% utilization is considered ideal.

Why the 30% Rule Matters

- Credit scoring models consider 30% utilization as healthy credit behavior.

- Using more than 30% of your available credit can lower your score.

- Using too little credit (like 10% or less) may also show lenders that you have limited credit activity.

Tip: Aim to keep your balance around 30% of your total credit limit.

High vs Low Utilization: What It Means for Your Score

| Utilization | Impact on Credit Score |

|---|---|

| 0–10% | Safe, but low activity may slightly limit score growth |

| 10–30% | Ideal, positive impact |

| 30–50% | Score may drop slightly |

| 50%+ | Score likely negatively affected, higher risk |

Practical Tips to Lower Your Utilization and Boost Score

1. Pay Balances Before Statement Closing Date

- Paying off your balance before the statement date lowers your reported utilization.

- Example: If you use $1,500 but pay $500 before the statement, your utilization drops immediately.

2. Use Multiple Cards Wisely

- Spreading purchases across several cards keeps individual card utilization lower and improves overall ratio.

3. Request a Credit Limit Increase

- Increasing your credit limit without increasing your spending lowers utilization naturally.

- Example: $5,000 limit → $7,500 limit; $1,500 balance → utilization drops from 30% to 20%.

4. Don’t Close Old Cards

- Closing older accounts reduces your total available credit, which can increase utilization ratio.

5. Track Your Credit Regularly

- Use apps like Credit Karma, Experian, or Mint to monitor utilization and overall credit health.

6. Spend Smartly

- Avoid using a large percentage of your credit for non-essential expenses. Plan large purchases and pay them off quickly.

Common Mistakes to Avoid

- Carrying high balances past the statement date

- Overusing a single credit card

- Opening too many new cards at once

- Making only minimum payments

FAQs

Q1: What is the ideal credit card utilization ratio in the US?

A: Keep it around 30% or lower.

Q2: Will my score drop if I use 50% of my credit?

A: Yes, higher utilization typically negatively affects your credit score.

Q3: Do multiple credit cards help improve utilization?

A: Yes, spreading balances across multiple cards reduces overall utilization.

Q4: How can I easily track my utilization?

A: Free tools like Credit Karma, Experian, or Mint help you monitor your utilization and score.

Q5: How quickly does utilization impact my score?

A: Usually within 1–2 billing cycles after the reported balance.

Final Thoughts

Managing your credit card utilization ratio is one of the fastest ways to boost your credit score in the US. Following the 30% rule helps:

- Improve your credit score

- Show positive credit behavior to lenders

- Keep long-term financial health strong

Remember, utilization is only one part of your credit score. Timely payments, responsible card use, and maintaining old accounts are equally important.